What’s the state of spatial computing? As we enter a new year, we embark on our annual exercise to define the sector, its players, events, and trajectory. This year, we ended up with almost 100 pages of analysis. To maintain our persistent goal to achieve analytical depth, we’ve split the report into two parts, rather than scale it back. The pages that follow represent Part 1, with Part 2 to follow next month.

As for findings, XR continues to push forward while its biggest players invest tens of billions collectively to realize their self-centric versions of a spatial future. But though self serving, these players accelerate XR in the aggregate as they fund the industry’s expansion, R&D, marketing, and consumer education.

For example, Meta’s spending spree in its Reality Labs division – though recently scaled back to a degree – has struck the right chord with Ray-Ban Meta Smartglasses (RBMS). The device balances technology and style in ways that meet consumers’ current XR appetites. In other words, they’re more eyewear than technology. This formula, though it has proved elusive to tech giants over the past decade, has been validated through RBMS consumer traction. The market has spoken, to the tune of 5 million+ lifetime units sold. Moreover, they’ve signaled a model for the right UX balance between visuals and AI.

Sticking with that last point, the intelligence and utility that AI brings to the table lessen AR’s reliance on visuals as a selling point. It rather offers intelligent functions such as personal alerts, social signals, shopping & commerce, and world annotation. This utility is met with the style and wearability that’s possible when you sidestep AR display systems.

But this AI-reliant and AR-lite approach isn’t a silver bullet. It’s just one of many paths being forged today. And that device divergence is a mark of an industry moving into adolescence. Indeed, a variety of purpose-built and app-dependent form factors will unlock value and greater appeal than the do-everything bulk that characterized AR’s previous generation of flagships. Where will those divergent paths take us? Who’s best positioned? And where do VR and mobile AR sit in all this? We’ll tackle these questions through numbers and narratives.

The fastest and most cost-efficient way to get access to this report is by subscribing to ARtillery PRO. You can also purchase it a la carte (the purchase of this report includes Part 2 of the series).

ARtillery Intelligence follows disciplined best practices in market sizing and forecasting, developed and reinforced through its principles’ 20 years in research and intelligence in tech sectors. This includes the past 10 years covering AR & VR as a primary focus.

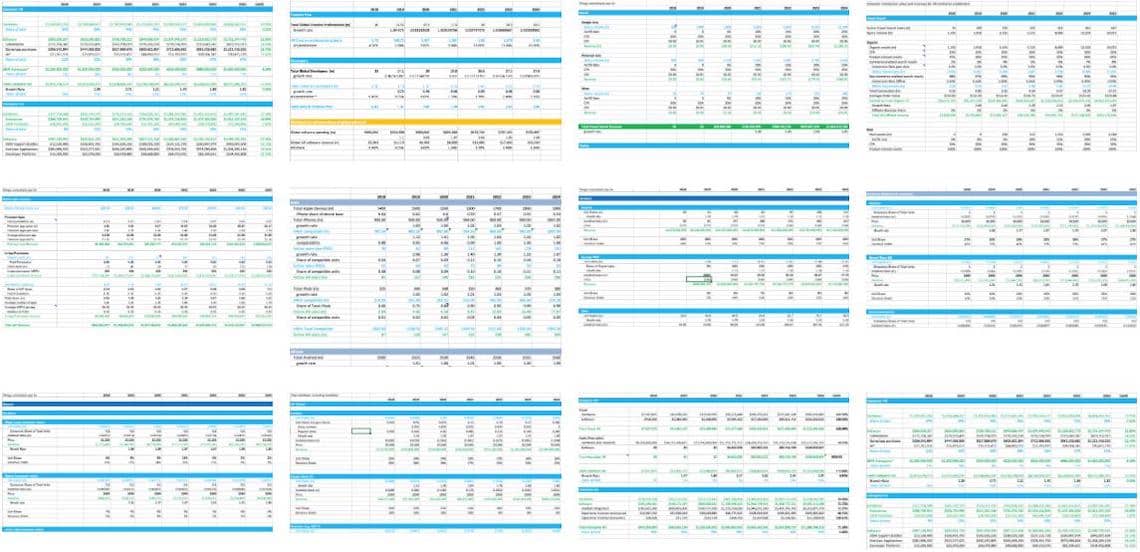

This report focuses on revenue projections in various sub-sectors and product areas. ARtillery Intelligence has built financial models that are customized to the specific dynamics and unit economics of each. These include variables like unit sales, company revenues, pricing trends, market trajectory, and several other micro and macro factors that ARtillery Intelligence tracks.

This approach primarily applies a bottom-up forecasting methodology, which is secondarily vetted against a top-down analysis. Together, confidence is achieved through triangulating revenues and projections in a disciplined way. More about ARtillery Intelligence’s market-sizing methodology can be seen here and more on its credentials can be seen here.

Unless specified in its stock ownership disclosures, ARtillery Intelligence has no financial stake in the companies mentioned in its reports. The production of this report likewise wasn’t commissioned. With all market sizing, ARtillery Intelligence remains independent of players and practitioners in the sectors it covers, thus mitigating bias in industry revenue calculations and projections. ARtillery Intelligence’s disclosures, stock ownership, and ethics policy can be seen in full here.

Checkout easily and securely.

Ask us anything

Credentials & context