The latest original intelligence. Subscribers, log in for full access.

Monthly reports since 2017. Subscribers, log in for full access.

Latest

Latest

Archive

Latest

Archive

What’s coming up…

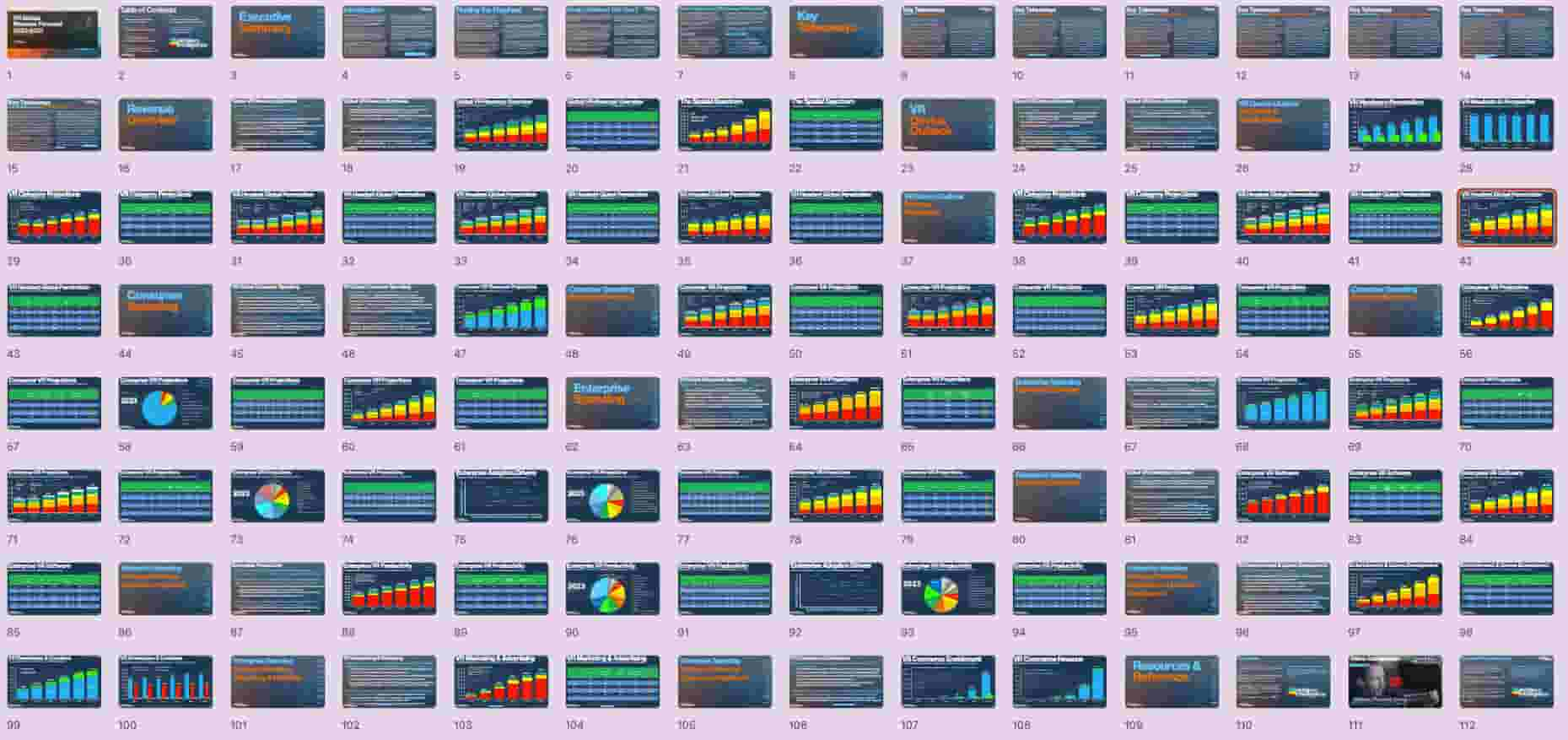

August Report – Enterprise XR Best Practices & Case Studies, Volume 5

September Report – Spatial Revenue Forecast: Q3 Update

October Report – AR Glasses: Gaming Out the Near Term Market

Gain access to the entire intelligence vault.

For those working in #XR and others looking to educate yourselves on this industry ditch the Wave reports and Hype Cycles and opt for a specialist industry analyst firm. Michael Boland’s team at ARtillery Intelligence delivers original, relevant and well prepped/delivered insights and data analytics on the market trends that matter across the extended reality ecosystem.

Reynaldo Zabala

XR Strategy Director / RazorEdge